0050.XGB.180D. 1'st.practice

2024-06-19

!pip install yfinance

import yfinance as yf

# 下載0050過去5年的股價數據

ticker = '0050.TW'

stock_data = yf.download(ticker, period='5y')

stock_data.reset_index(inplace=True)

stock_data.to_csv('0050_stock_data.csv', index=False)

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from sklearn.preprocessing import MinMaxScaler

import tensorflow as tf

from tensorflow.keras.models import Sequential

from tensorflow.keras.layers import Dense, LSTM

from sklearn.metrics import mean_squared_error

import math

# 加載數據

df = pd.read_csv('0050_stock_data.csv')

df = df[['Date', 'Close']]

# 數據歸一化

scaler = MinMaxScaler(feature_range=(0, 1))

df_scaled = scaler.fit_transform(df[['Close']])

# 創建訓練和測試集

train_size = int(len(df_scaled) * 0.8)

test_size = len(df_scaled) - train_size

train_data, test_data = df_scaled[0:train_size, :], df_scaled[train_size:len(df_scaled), :]

# 創建數據集

def create_dataset(dataset, time_step=1):

dataX, dataY = [], []

for i in range(len(dataset) - time_step - 1):

a = dataset[i:(i + time_step), 0]

dataX.append(a)

dataY.append(dataset[i + time_step, 0])

return np.array(dataX), np.array(dataY)

time_step = 100

X_train, Y_train = create_dataset(train_data, time_step)

X_test, Y_test = create_dataset(test_data, time_step)

# 調整數據格式以適應LSTM輸入

X_train = X_train.reshape(X_train.shape[0], X_train.shape[1], 1)

X_test = X_test.reshape(X_test.shape[0], X_test.shape[1], 1)

# 構建LSTM模型

model = Sequential()

model.add(LSTM(50, return_sequences=True, input_shape=(time_step, 1)))

model.add(LSTM(50, return_sequences=False))

model.add(Dense(25))

model.add(Dense(1))

# 編譯模型

model.compile(optimizer='adam', loss='mean_squared_error')

# 訓練模型

model.fit(X_train, Y_train, batch_size=1, epochs=10)

import matplotlib.dates as mdates

# 確保日期列的格式正確

df['Date'] = pd.to_datetime(df['Date'])

# 預測數據

train_predict = model.predict(X_train)

test_predict = model.predict(X_test)

# 反歸一化預測結果

train_predict = scaler.inverse_transform(train_predict)

test_predict = scaler.inverse_transform(test_predict)

Y_train = scaler.inverse_transform(np.array(Y_train).reshape(-1, 1))

Y_test = scaler.inverse_transform(np.array(Y_test).reshape(-1, 1))

# 計算RMSE

train_rmse = math.sqrt(mean_squared_error(Y_train, train_predict))

test_rmse = math.sqrt(mean_squared_error(Y_test, test_predict))

print(f'Train RMSE: {train_rmse}')

print(f'Test RMSE: {test_rmse}')

# 繪製訓練數據的預測結果

train_predict_plot = np.empty_like(df_scaled)

train_predict_plot[:, :] = np.nan

train_predict_plot[time_step:len(train_predict) + time_step, :] = train_predict

# 繪製測試數據的預測結果

test_predict_plot = np.empty_like(df_scaled)

test_predict_plot[:, :] = np.nan

test_predict_plot[len(train_predict) + (time_step * 2) + 1:len(df_scaled) - 1, :] = test_predict

# 預測未來180天

future_days = 180

temp_input = list(test_data[-time_step:].flatten())

# 確保 temp_input 的長度正確

assert len(temp_input) == time_step, f"temp_input 的長度不正確:{len(temp_input)},應該是 {time_step}"

# 迭代預測未來的數據

future_predictions = []

for i in range(future_days):

if len(temp_input) > time_step:

temp_input = temp_input[-time_step:]

try:

input_data = np.array(temp_input).reshape((1, time_step, 1))

except ValueError as e:

print(f"Error at iteration {i}: {e}")

print(f"temp_input: {temp_input}")

break

future_prediction = model.predict(input_data)

temp_input.append(future_prediction[0][0])

future_predictions.append(future_prediction[0][0])

# 反歸一化未來預測結果

if len(future_predictions) > 0: # 確保有未來的預測結果

future_predictions = scaler.inverse_transform(np.array(future_predictions).reshape(-1, 1))

# 繪製結果

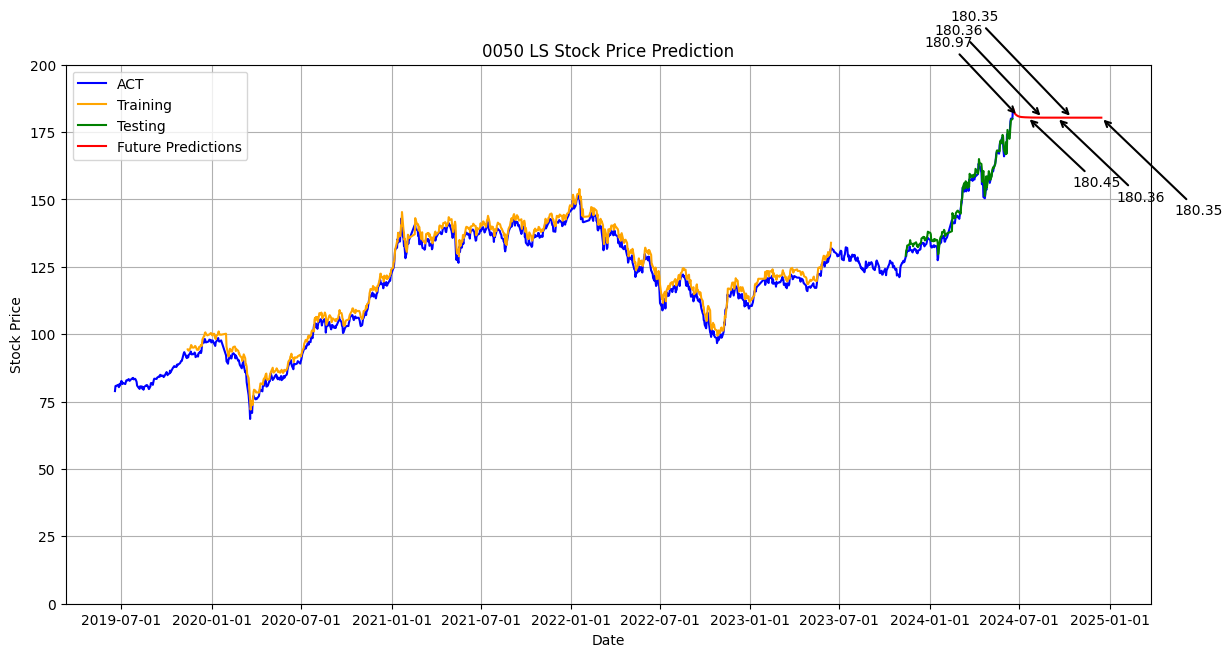

plt.figure(figsize=(14, 7))

plt.plot(df['Date'], scaler.inverse_transform(df_scaled), label='ACT', color='blue')

plt.plot(df['Date'], train_predict_plot, label='Training', color='orange')

plt.plot(df['Date'], test_predict_plot, label='Testing', color='green')

# 繪製未來180天的預測結果

future_dates = pd.date_range(start=df['Date'].iloc[-1], periods=future_days + 1).tolist()

plt.plot(future_dates[1:], future_predictions, label='Future Predictions', color='red')

# 標示特定日期的收盤價

specific_days = [10, 30, 60, 90, 120, 180]

offsets = [(-50, 50), (50, -50), (-60, 60), (60, -60), (-70, 70), (70, -70)] # 进一步增加间距

for i, day in enumerate(specific_days):

plt.annotate(f'{future_predictions[day-1][0]:.2f}',

(future_dates[day], future_predictions[day-1]),

textcoords="offset points",

xytext=offsets[i],

ha='center',

arrowprops=dict(arrowstyle='->', lw=1.5, color='black'),

color='black')

# 設置 x 軸標記為每半年

ax = plt.gca()

ax.xaxis.set_major_locator(mdates.MonthLocator(bymonth=[1, 7], bymonthday=1))

ax.xaxis.set_major_formatter(mdates.DateFormatter('%Y-%m-%d'))

# 設置 y 軸範圍

plt.ylim(0, 200)

plt.xlabel('Date')

plt.ylabel('Stock Price')

plt.title('0050 LS Stock Price Prediction')

plt.legend(loc='upper left')

plt.grid(True)

plt.show()

else:

print("No future predictions to plot.")