import pandas as pd

import matplotlib.pyplot as plt

import numpy as np

from sklearn.preprocessing import MinMaxScaler

from sklearn.metrics import mean_squared_error

import math

import xgboost as xgb # 確保導入 XGBoost

from sklearn.model_selection import GridSearchCV

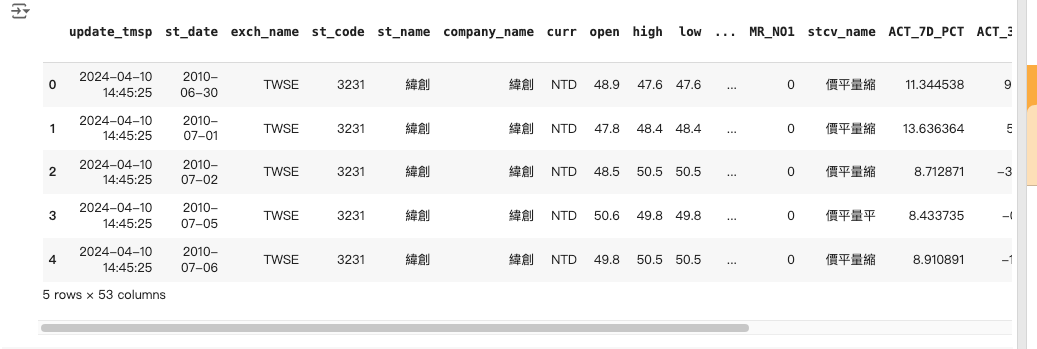

df = pd.read_csv('/content/3231_0614t.csv')

df.head()

# 重置索引提取 'Close' 列

df['st_date'] = pd.to_datetime(df['st_date'])

df2 = df.reset_index()[['st_date', 'close']]

# 建更多特徵

df2['Year'] = df2['st_date'].dt.year

df2['Month'] = df2['st_date'].dt.month

df2['Weekday'] = df2['st_date'].dt.weekday

df2['MA5'] = df2['close'].rolling(window=5).mean()

df2['MA10'] = df2['close'].rolling(window=10).mean()

df2['MA20'] = df2['close'].rolling(window=20).mean()

df2 = df2.dropna()

# 創建數據集

train_size = int(len(df2_scaled) * 0.65)

test_size = len(df2_scaled) - train_size

train_data, test_data = df2_scaled[0:train_size, :], df2_scaled[train_size:len(df2_scaled), :]

# 數據集

def create_dataset(dataset, time_step=1):

dataX, dataY = [], []

for i in range(len(dataset) - time_step - 1):

a = dataset[i:(i + time_step), :]

dataX.append(a)

dataY.append(dataset[i + time_step, 0]) # 預測 'close' 列

return np.array(dataX), np.array(dataY)

time_step = 100

X_train, Y_train = create_dataset(train_data, time_step)

X_test, Y_test = create_dataset(test_data, time_step)

# XGBoost的格式

X_train = X_train.reshape(X_train.shape[0], -1)

X_test = X_test.reshape(X_test.shape[0], -1)

# XGBoost模型和参數

xg_reg = xgb.XGBRegressor(objective='reg:squarederror', missing=np.nan)

param_grid = {

'colsample_bytree': [0.3, 0.5, 0.7],

'learning_rate': [0.01, 0.1, 0.2],

'max_depth': [3, 5, 7],

'n_estimators': [100, 200, 300],

'subsample': [0.6, 0.8, 1.0],

'gamma': [0, 0.1, 0.2]

}

# 進進網格搜索

grid_search = GridSearchCV(estimator=xg_reg, param_grid=param_grid, scoring='neg_mean_squared_error', cv=3, verbose=1)

grid_search.fit(X_train, Y_train)

# 穫取最佳参数

best_params = grid_search.best_params_

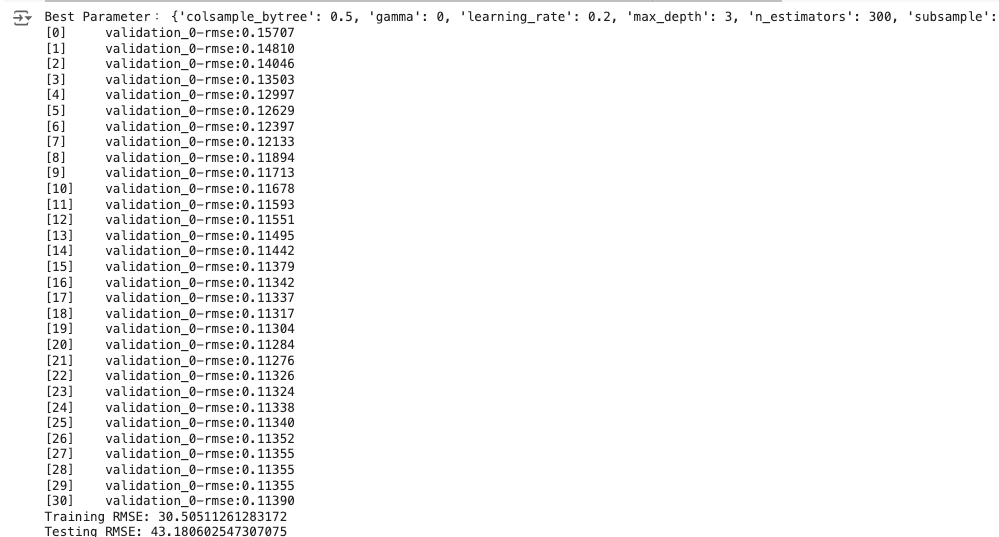

print("Best Parameter:", best_params)

# 使用最佳参数訓練模型

xg_reg_best = xgb.XGBRegressor(**best_params, early_stopping_rounds=10, eval_metric='rmse')

xg_reg_best.fit(X_train, Y_train, eval_set=[(X_test, Y_test)], verbose=True)

# 預測

train_predict = xg_reg_best.predict(X_train)

test_predict = xg_reg_best.predict(X_test)

# 反歸一化預測結果

train_predict_inverse = scaler.inverse_transform(train_data[time_step:len(train_predict) + time_step, :]) # Pass the original training data with all features

test_predict_inverse = scaler.inverse_transform(test_data[time_step:len(test_predict) + time_step, :]) # Pass the original testing data with all features

# Extract the 'close' column for RMSE calculation

train_predict = train_predict_inverse[:, 0]

test_predict = test_predict_inverse[:, 0]

# 計算RMSE

rmse_train = math.sqrt(mean_squared_error(Y_train, train_predict))

print("Training RMSE:", rmse_train)

rmse_test = math.sqrt(mean_squared_error(Y_test, test_predict))

print("Testing RMSE:", rmse_test)

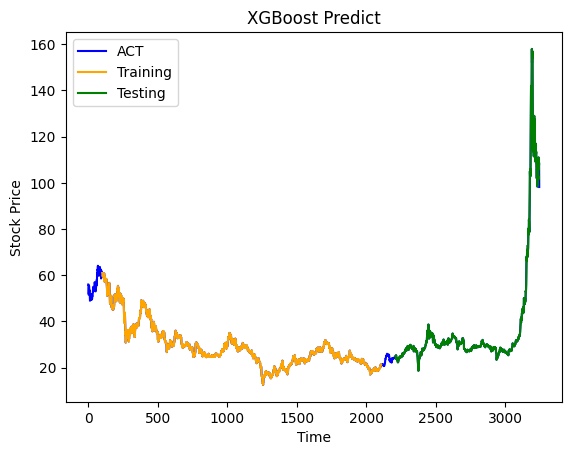

# 繪制預測結果

look_back = time_step

trainPredictPlot = np.empty_like(df2_scaled[:, 0])

trainPredictPlot[:] = np.nan

trainPredictPlot[look_back:len(train_predict) + look_back] = train_predict

testPredictPlot = np.empty_like(df2_scaled[:, 0])

testPredictPlot[:] = np.nan

testPredictPlot[len(train_predict) + (look_back * 2) + 1:len(df2_scaled) - 1] = test_predict

plt.plot(scaler.inverse_transform(df2_scaled)[:, 0], color='blue', label='ACT')

plt.plot(trainPredictPlot, color='orange', label='Training')

plt.plot(testPredictPlot, color='green', label='Testing')

plt.title('XGBoost Predict')

plt.xlabel('Time')

plt.ylabel('Stock Price')

plt.legend()

plt.show()