SVM.dft1.TAIEX.POC.0628

from google.colab import drive

drive.mount('/content/drive')

!pip install yfinance scikit-learn matplotlib statsmodels ta

import yfinance as yf

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from sklearn.preprocessing import MinMaxScaler

from sklearn.svm import SVR

from sklearn.decomposition import PCA

from sklearn.metrics import mean_squared_error, mean_absolute_error, roc_curve, roc_auc_score

from sklearn.model_selection import GridSearchCV

import statsmodels.api as sm

import ta

# 計算 Chande Momentum Oscillator (CMO)

def calculate_cmo(data, window):

delta = data.diff()

up = delta.where(delta > 0, 0.0)

down = -delta.where(delta < 0, 0.0)

sum_up = up.rolling(window=window).sum()

sum_down = down.rolling(window=window).sum()

cmo = 100 * (sum_up - sum_down) / (sum_up + sum_down)

return cmo

# 下載數據

tickers = ['2330.TW', '2454.TW', '2317.TW', '2412.TW', '1303.TW', '2882.TW',

'3008.TW', '2308.TW', '1402.TW', '1216.TW', '2881.TW', '2891.TW',

'2382.TW', '2409.TW', '1802.TW', '1101.TW', '3045.TW', '2324.TW',

'2105.TW', '2880.TW', '2887.TW', '2885.TW', '4904.TW', '2603.TW',

'2884.TW', '2886.TW', '2357.TW', '2344.TW', '4938.TW', '2888.TW', '^TWII']

data = yf.download(tickers, start="2021-01-01", end="2024-06-28")

adj_close = data['Adj Close']

high = data['High']

low = data['Low']

# 計算技術指標

features = pd.DataFrame(index=adj_close.index)

twii_returns = adj_close['^TWII'].pct_change()

for ticker in tickers[:-1]: # 不包括 '^TWII'

stock_returns = adj_close[ticker].pct_change()

cov_matrix = stock_returns.rolling(window=120).cov(twii_returns)

var = twii_returns.rolling(window=120).var()

features[f'{ticker}_beta'] = cov_matrix / var

features[f'{ticker}_MA7'] = adj_close[ticker].rolling(window=7).mean()

features[f'{ticker}_RSI14'] = ta.momentum.RSIIndicator(close=adj_close[ticker], window=14).rsi()

features[f'{ticker}_Bollinger_upper'] = ta.volatility.BollingerBands(close=adj_close[ticker], window=20, window_dev=2).bollinger_hband()

features[f'{ticker}_Bollinger_lower'] = ta.volatility.BollingerBands(close=adj_close[ticker], window=20, window_dev=2).bollinger_lband()

features[f'{ticker}_Aroon_up'] = ta.trend.AroonIndicator(high=high[ticker], low=low[ticker], window=25).aroon_up()

features[f'{ticker}_Aroon_down'] = ta.trend.AroonIndicator(high=high[ticker], low=low[ticker], window=25).aroon_down()

features[f'{ticker}_CCI'] = ta.trend.CCIIndicator(high=high[ticker], low=low[ticker], close=adj_close[ticker], window=20).cci()

features[f'{ticker}_CMO'] = calculate_cmo(adj_close[ticker], window=14)

features[f'{ticker}_WILLR'] = ta.momentum.WilliamsRIndicator(high=high[ticker], low=low[ticker], close=adj_close[ticker], lbp=14).williams_r()

# 移除 P 值大於 0.05 的變數

X = features.dropna()

y = adj_close['^TWII'].loc[X.index.to_list()]

# 標準化

scaler = MinMaxScaler()

X_scaled = scaler.fit_transform(X)

# PCA 降維

pca = PCA(n_components=0.95) # 保留 95% 的方差

X_pca = pca.fit_transform(X_scaled)

# OLS 回歸

X_pca_const = sm.add_constant(X_pca)

model = sm.OLS(y, X_pca_const).fit()

print(model.summary())

# 分割數據集

train_size = 0.8

train_index = int(len(X_pca) * train_size)

X_train_pca, X_test_pca = X_pca[:train_index], X_pca[train_index:]

y_train, y_test = y[:train_index], y[train_index:]

# 支持向量機回歸

param_grid = {

'C': [0.1, 1, 10, 100],

'gamma': [1, 0.1, 0.01, 0.001],

'epsilon': [0.1, 0.2, 0.5, 0.3],

'kernel': ['rbf']

}

grid_search = GridSearchCV(SVR(), param_grid, refit=True, cv=5, n_jobs=-1)

grid_search.fit(X_train_pca, y_train)

# 預測

train_predict = grid_search.predict(X_train_pca)

test_predict = grid_search.predict(X_test_pca)

# 限制每日最大漲跌幅為 10%

def limit_change(predictions, previous_value, max_change=0.1):

limited_predictions = []

for pred in predictions:

change = (pred - previous_value) / previous_value

if change > max_change:

pred = previous_value * (1 + max_change)

elif change < -max_change:

pred = previous_value * (1 - max_change)

limited_predictions.append(pred)

previous_value = pred

return np.array(limited_predictions)

# 應用漲跌幅限制

train_predict = limit_change(train_predict, y_train.iloc[0])

test_predict = limit_change(test_predict, y_test.iloc[0])

# 計算 MSE 和 MAE

train_mse = mean_squared_error(y_train, train_predict)

test_mse = mean_squared_error(y_test, test_predict)

train_mae = mean_absolute_error(y_train, train_predict)

test_mae = mean_absolute_error(y_test, test_predict)

print(f"Training MSE: {train_mse:.4f}")

print(f"Testing MSE: {test_mse:.4f}")

print(f"Training MAE: {train_mae:.4f}")

print(f"Testing MAE: {test_mae:.4f}")

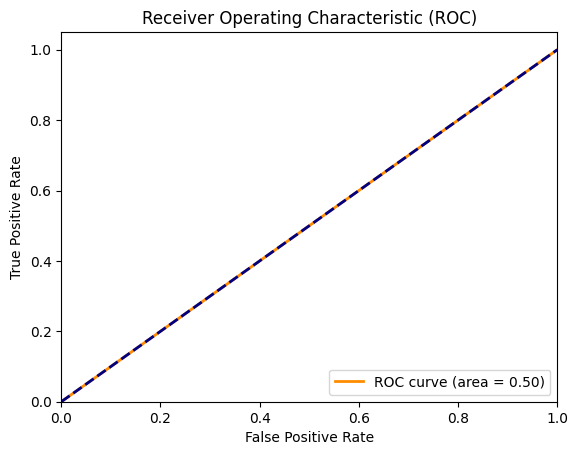

# 二元分類

threshold = np.median(y_test) # 設定閾值為測試數據的中位數

y_test_class = (y_test > threshold).astype(int)

test_predict_class = (test_predict > threshold).astype(int)

# 確保有兩個類別

if len(np.unique(y_test_class)) > 1:

# 計算 ROC 曲線和 AUC 值

fpr, tpr, _ = roc_curve(y_test_class, test_predict_class)

roc_auc = roc_auc_score(y_test_class, test_predict_class)

# 繪製 ROC 曲線

plt.figure()

plt.plot(fpr, tpr, color='darkorange', lw=2, label='ROC curve (area = %0.2f)' % roc_auc)

plt.plot([0, 1], [0, 1], color='navy', lw=2, linestyle='--')

plt.xlim([0.0, 1.0])

plt.ylim([0.0, 1.05])

plt.xlabel('False Positive Rate')

plt.ylabel('True Positive Rate')

plt.title('Receiver Operating Characteristic (ROC)')

plt.legend(loc="lower right")

plt.show()

else:

print("ROC AUC score is not defined as there is only one class present in y_test_class.")

# 繪製整個數據集的走勢圖

plt.figure(figsize=(14, 7))

plt.plot(y_train.index, y_train, color='blue', label='ACTUAL')

plt.plot(y_train.index, train_predict, color='orange', label='Training')

plt.plot(y_test.index, y_test, color='blue')

plt.plot(y_test.index, test_predict, color='red', label='Prediction')

plt.legend() # 確保圖例顯示

plt.xlabel('Date')

plt.ylabel('TAIEX')

plt.title('TAIEX Prediction')

plt.grid(True)

plt.show()

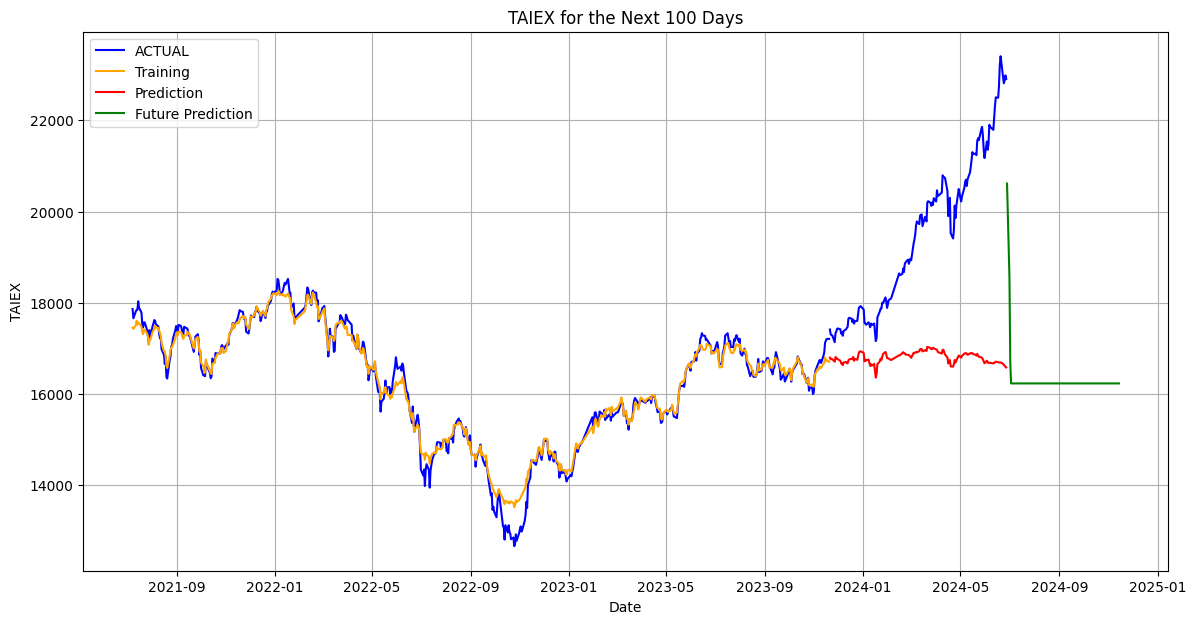

# 預測未來 100 天的走勢

future_dates = pd.date_range(start=y_test.index[-1], periods=101, freq='B')[1:]

future_features = X_test_pca[-1:].copy()

future_predictions = []

for i in range(100):

next_day = grid_search.best_estimator_.predict(future_features.reshape(1, -1))[0]

future_predictions.append(next_day)

next_day_features = np.array([next_day] * future_features.shape[1]).reshape(1, -1)

future_features = np.append(future_features[1:], next_day_features, axis=0)

# 應用漲跌幅限制

future_predictions = limit_change(future_predictions, y_test.iloc[-1])

# 顯示未來 100 天的預測結果

plt.figure(figsize=(14, 7))

plt.plot(y_train.index, y_train, color='blue', label='ACTUAL')

plt.plot(y_train.index, train_predict, color='orange', label='Training')

plt.plot(y_test.index, y_test, color='blue')

plt.plot(y_test.index, test_predict, color='red', label='Prediction')

plt.plot(future_dates, future_predictions, color='green', label='Future Prediction')

plt.legend() # 確保圖例顯示

plt.xlabel('Date')

plt.ylabel('TAIEX')

plt.title('TAIEX for the Next 100 Days')

plt.grid(True)

plt.show()

基本變數

Adj Close: 股票的調整收盤價

High: 股票的最高價

Low: 股票的最低價

計算出的技術指標變數

beta: 股票的 Beta 值(與台灣加權指數的協方差除以台灣加權指數的方差)

MA7: 7 天移動平均線

RSI14: 14 天相對強弱指數

Bollinger_upper: 布林帶上軌

Bollinger_lower: 布林帶下軌

Aroon_up: Aroon 指標中的上升線

Aroon_down: Aroon 指標中的下降線

CCI: 商品通道指標

CMO: Chande 動量擺動指標

WILLR: 威廉指數

使用的技術指標變數(每個股票的技術指標變數前綴為股票代碼)

例如:

2330.TW_beta

2330.TW_MA7

2330.TW_RSI14

2330.TW_Bollinger_upper

2330.TW_Bollinger_lower

2330.TW_Aroon_up

2330.TW_Aroon_down

2330.TW_CCI

2330.TW_CMO

2330.TW_WILLR

同樣地,其他股票的變數名稱也遵循相同的命名方式,例如 2454.TW_beta、2454.TW_MA7 等等。

目標變數

y: 台灣加權指數 (^TWII) 的調整收盤價。

PCA 降維

PCA 將高維度的特徵空間降維到保留 95% 方差的低維空間。具體的變數數量取決於原始特徵的數量和數據的內在結構。

OLS 回歸中的變數

在進行 OLS 回歸時,我們會對經過標準化和 PCA 降維後的變數進行回歸。這些變數經過降維後變成了主成分變數(Principal Components)。

具體到這個代碼中,我們使用的變數總數(原始特徵)會很多,但經過 PCA 降維後實際使用的變數數量會減少,保留了最重要的幾個主成分。

變數摘要

- 基本變數:

Adj Close、High、Low - 技術指標變數:

beta、MA7、RSI14、Bollinger_upper、Bollinger_lower、Aroon_up、Aroon_down、CCI、CMO、WILLR - 使用的技術指標變數(每個股票的技術指標變數前綴為股票代碼):

2330.TW_beta、2330.TW_MA7、2330.TW_RSI14、2330.TW_Bollinger_upper、2330.TW_Bollinger_lower、2330.TW_Aroon_up、2330.TW_Aroon_down、2330.TW_CCI、2330.TW_CMO、2330.TW_WILLR- 其他股票變數名稱也遵循相同的命名方式

- 目標變數:台灣加權指數 (^TWII) 的調整收盤價

adj_close['^TWII'] - PCA 降維後的主成分變數:使用 PCA 降維後的主成分變數

這些變數經過降維後成為主成分變數,並應用於 OLS 回歸和支持向量機回歸中。