0050.XGB.2nd.practice

2024-06-19

# 安裝必要的庫 XGB

!pip install yfinance xgboost

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import yfinance as yf

from sklearn.preprocessing import MinMaxScaler

from sklearn.metrics import mean_squared_error

import xgboost as xgb

import math

# 下載0050過去5年的股價數據

ticker = '0050.TW'

stock_data = yf.download(ticker, period='5y')

stock_data.reset_index(inplace=True)

stock_data.to_csv('0050_stock_data.csv', index=False)

# 加載數據

df = pd.read_csv('0050_stock_data.csv')

df = df[['Date', 'Close']]

# 數據歸一化

scaler = MinMaxScaler(feature_range=(0, 1))

df_scaled = scaler.fit_transform(df[['Close']])

# 創建訓練和測試集

train_size = int(len(df_scaled) * 0.8)

test_size = len(df_scaled) - train_size

train_data, test_data = df_scaled[0:train_size, :], df_scaled[train_size:len(df_scaled), :]

# 創建數據集

def create_dataset(dataset, time_step=1):

dataX, dataY = [], []

for i in range(len(dataset) - time_step - 1):

a = dataset[i:(i + time_step), 0]

dataX.append(a)

dataY.append(dataset[i + time_step, 0])

return np.array(dataX), np.array(dataY)

time_step = 100

X_train, Y_train = create_dataset(train_data, time_step)

X_test, Y_test = create_dataset(test_data, time_step)

# 構建XGBoost模型

model = xgb.XGBRegressor(objective='reg:squarederror', n_estimators=100, learning_rate=0.1, max_depth=5)

# 訓練模型

model.fit(X_train, Y_train)

# 預測數據

train_predict = model.predict(X_train)

test_predict = model.predict(X_test)

# 反歸一化預測結果

train_predict = scaler.inverse_transform(train_predict.reshape(-1, 1))

test_predict = scaler.inverse_transform(test_predict.reshape(-1, 1))

Y_train = scaler.inverse_transform(Y_train.reshape(-1, 1))

Y_test = scaler.inverse_transform(Y_test.reshape(-1, 1))

# 計算RMSE

train_rmse = math.sqrt(mean_squared_error(Y_train, train_predict))

test_rmse = math.sqrt(mean_squared_error(Y_test, test_predict))

print(f'Train RMSE: {train_rmse}')

print(f'Test RMSE: {test_rmse}')

# 繪製結果

import matplotlib.dates as mdates

# 確保日期列的格式正確

df['Date'] = pd.to_datetime(df['Date'])

# 繪製訓練數據的預測結果

train_predict_plot = np.empty_like(df_scaled)

train_predict_plot[:, :] = np.nan

train_predict_plot[time_step:len(train_predict) + time_step, :] = train_predict

# 繪製測試數據的預測結果

test_predict_plot = np.empty_like(df_scaled)

test_predict_plot[:, :] = np.nan

test_predict_plot[len(train_predict) + (time_step * 2) + 1:len(df_scaled) - 1, :] = test_predict

# 預測未來180天

future_days = 180

temp_input = list(test_data[-time_step:].flatten())

# 確保 temp_input 的長度正確

assert len(temp_input) == time_step, f"temp_input 的長度不正確:{len(temp_input)},應該是 {time_step}"

# 迭代預測未來的數據

future_predictions = []

for i in range(future_days):

if len(temp_input) > time_step:

temp_input = temp_input[-time_step:]

try:

input_data = np.array(temp_input).reshape((1, time_step))

except ValueError as e:

print(f"Error at iteration {i}: {e}")

print(f"temp_input: {temp_input}")

break

future_prediction = model.predict(input_data)

temp_input.append(future_prediction[0])

future_predictions.append(future_prediction[0])

# 反歸一化未來預測結果

if len(future_predictions) > 0: # 確保有未來的預測結果

future_predictions = scaler.inverse_transform(np.array(future_predictions).reshape(-1, 1))

# 繪製結果

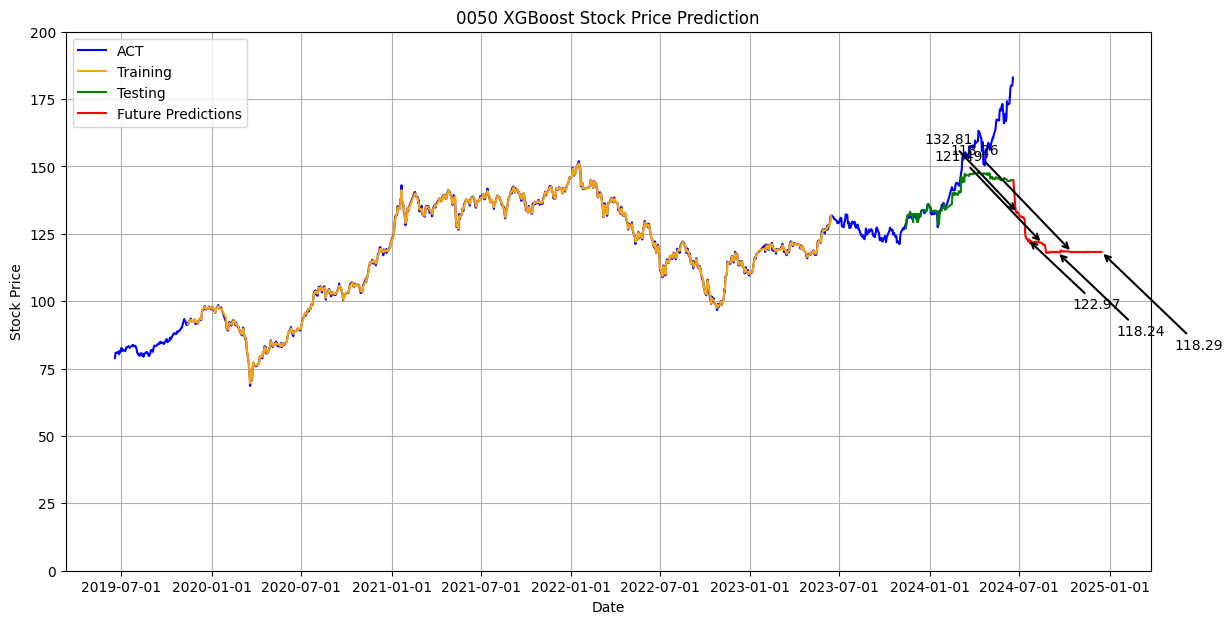

plt.figure(figsize=(14, 7))

plt.plot(df['Date'], scaler.inverse_transform(df_scaled), label='ACT', color='blue')

plt.plot(df['Date'], train_predict_plot, label='Training', color='orange')

plt.plot(df['Date'], test_predict_plot, label='Testing', color='green')

# 繪製未來180天的預測結果

future_dates = pd.date_range(start=df['Date'].iloc[-1], periods=future_days + 1).tolist()

plt.plot(future_dates[1:], future_predictions, label='Future Predictions', color='red')

# 標示特定日期的收盤價

specific_days = [10, 30, 60, 90, 120, 180]

offsets = [(-50, 50), (50, -50), (-60, 60), (60, -60), (-70, 70), (70, -70)] # 进一步增加间距

for i, day in enumerate(specific_days):

plt.annotate(f'{future_predictions[day-1][0]:.2f}',

(future_dates[day], future_predictions[day-1]),

textcoords="offset points",

xytext=offsets[i],

ha='center',

arrowprops=dict(arrowstyle='->', lw=1.5, color='black'),

color='black')

# 設置 x 軸標記為每半年

ax = plt.gca()

ax.xaxis.set_major_locator(mdates.MonthLocator(bymonth=[1, 7], bymonthday=1))

ax.xaxis.set_major_formatter(mdates.DateFormatter('%Y-%m-%d'))

# 設置 y 軸範圍

plt.ylim(0, 200)

plt.xlabel('Date')

plt.ylabel('Stock Price')

plt.title('0050 XGBoost Stock Price Prediction')

plt.legend(loc='upper left')

plt.grid(True)

plt.show()

else:

print("No future predictions to plot.")